The "27% Interest" Illusion: Unmasking Instant Loan Apps

"27% ब्याज" का भ्रम: इंस्टेंट लोन ऐप्स की असली सच्चाई

"Get a personal loan instantly at a basic interest rate of just 12% to 14%!" We see these ads everywhere, but do they ever actually deliver those low rates?

Almost never.

"सिर्फ 12% से 14% की मूल ब्याज दर पर तुरंत पर्सनल लोन प्राप्त करें!" हम हर जगह ऐसे विज्ञापन देखते हैं, लेकिन क्या वे वास्तव में कभी इतनी कम दरें देते हैं?

लगभग कभी नहीं।

First, they approve you at a much higher "Stated Rate" (like 27%). Then, because of massive upfront processing fees and GST, that loan actually ends up costing you closer to a 45% to 50% Annualized Percentage Rate (APR)!

सबसे पहले, वे आपको बहुत अधिक "स्टेटेड रेट" (जैसे 27%) पर मंजूरी देते हैं। फिर, भारी अपफ्रंट प्रोसेसिंग फीस और GST की वजह से, वह लोन असल में आपको 45% से 50% Annualized Percentage Rate (APR) के करीब पड़ जाता है!

Today, we are doing a reality check on popular instant loan apps like KreditBee. We will decode a real-life loan screenshot, reveal the hidden math they don't want you to calculate, and give you a powerful tool to check the True Cost (APR) of any loan offer you receive.

आज हम KreditBee जैसे लोकप्रिय इंस्टेंट लोन ऐप्स का रियलिटी चेक कर रहे हैं। हम एक असली लोन स्क्रीनशॉट को डिकोड करेंगे, उस छिपे हुए गणित का खुलासा करेंगे जिसे वे नहीं चाहते कि आप कैलकुलेट करें, और आपको एक पावरफुल टूल देंगे जिससे आप अपने किसी भी लोन ऑफर की असली लागत (True APR) जान सकें।

Case Studyकेस स्टडी

Decoding the KreditBee Screenshot

KreditBee स्क्रीनशॉट को डिकोड करना

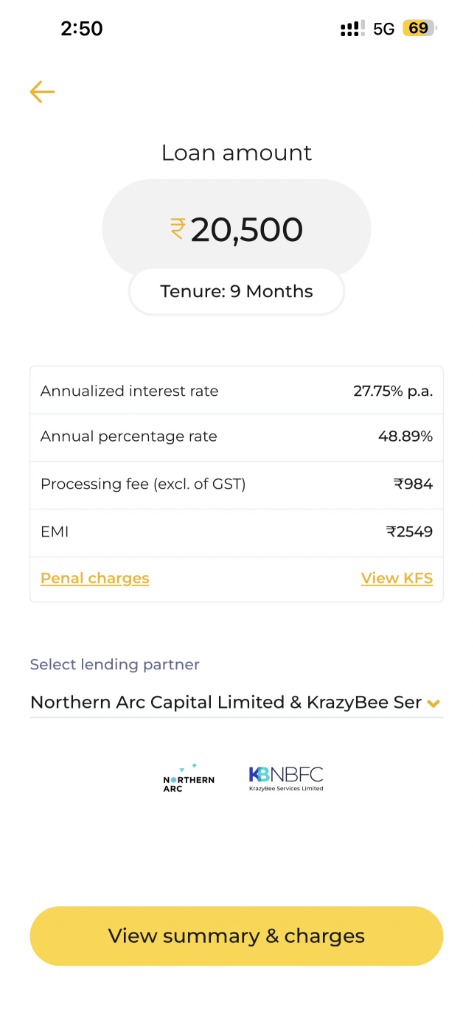

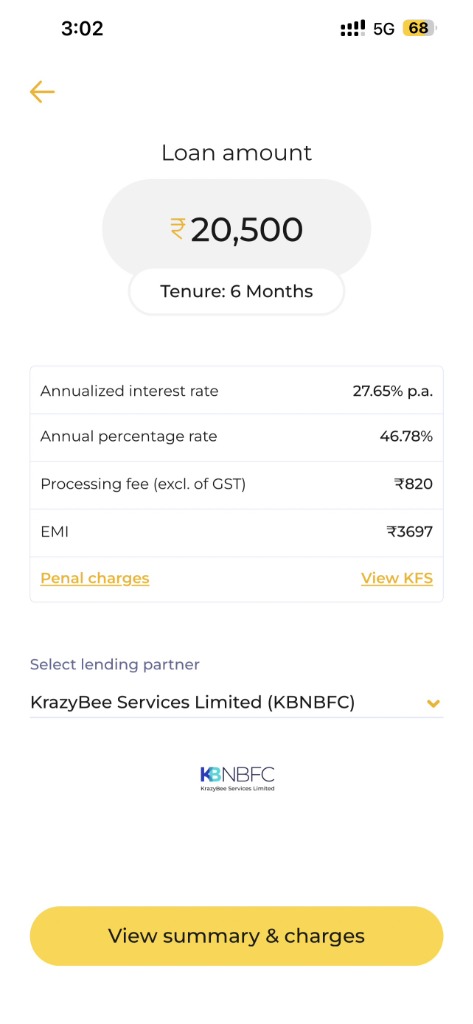

I am sharing my actual KreditBee loan offer screenshots with you below. Let's look at the numbers for a 9-month tenure and a 6-month tenure. The stated interest rate they offered me was around 27.75%, far above the "12% to 14%" advertised.

मैं आपके साथ नीचे अपने असली KreditBee लोन ऑफर के स्क्रीनशॉट शेयर कर रहा हूँ। आइए 9 महीने और 6 महीने की अवधि वाले लोन के आंकड़े देखते हैं। उन्होंने मुझे जो ब्याज दर दी थी वह 27.75% के आसपास थी, जो विज्ञापित "12% से 14%" से कहीं अधिक है।

| Metricपैमाना |

Valueवैल्यू |

| Loan Amount (Principal) |

₹20,500 |

| Stated Interest Rate (p.a.) |

27.75% |

| Monthly EMI |

₹2,549 |

| Total Repayment (EMI × 9) |

₹22,941 |

| Processing Fee + GST Deducted Upfront |

₹1,161 (₹984 + ₹177) |

| Estimated Net Disbursed (In Your Bank) |

₹19,339 |

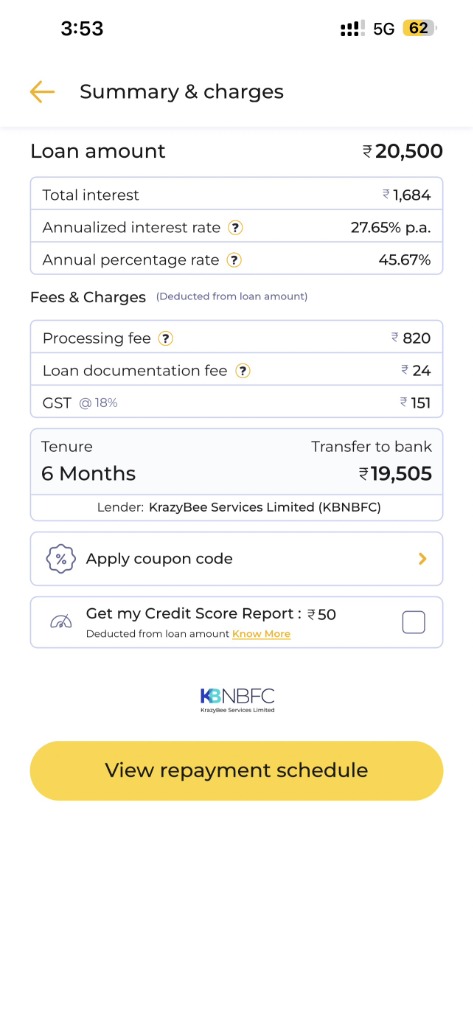

The Catchअसली जाल

You are paying EMI on ₹20,500. But you only received ₹19,339 in your bank account! Because the fee is deducted upfront, your principal is effectively lower, which drastically increases the mathematical cost of borrowing.

आप ₹20,500 पर EMI चुका रहे हैं। लेकिन आपको अपने बैंक खाते में सिर्फ ₹19,339 मिले! क्योंकि फीस पहले ही काट ली जाती है, इसलिए आपका असल मूलधन कम होता है, जो गणितीय रूप से उधार लेने की लागत को बहुत बढ़ा देता है।

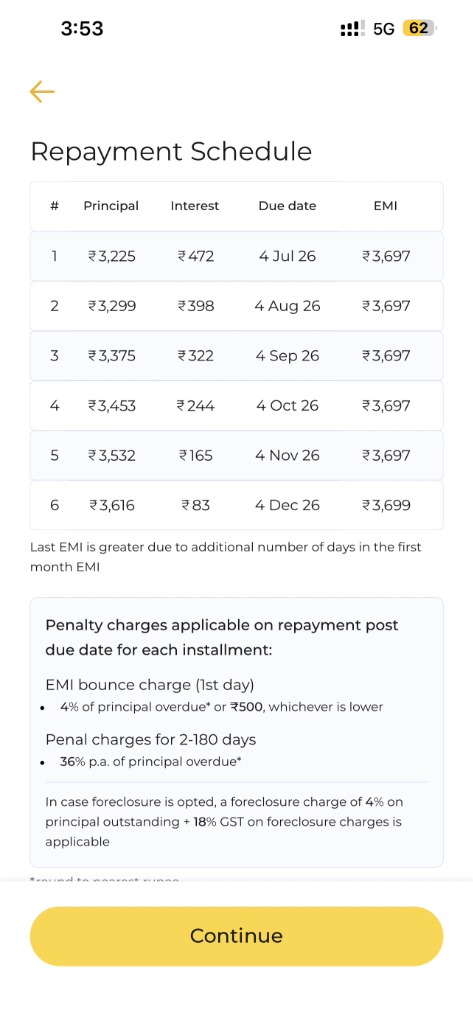

The Penalty Trap: 36% p.a. on Default

पेनल्टी ट्रैप: डिफ़ॉल्ट पर 36% p.a.

As if the 45%+ APR wasn't enough, look at their repayment schedule terms. If you miss an EMI, they hit you with a flat 4% bounce charge (or ₹500), PLUS a brutal 36% p.a. penal interest on the overdue amount. This is how people get trapped in a debt spiral.

मानो 45%+ APR कम था, उनकी पुनर्भुगतान अनुसूची की शर्तें देखें। यदि आप एक EMI चूक जाते हैं, तो वे आप पर 4% बाउंस चार्ज (या ₹500) लगाते हैं, साथ ही अतिदेय राशि पर 36% p.a. दंडात्मक ब्याज लगाते हैं। इसी तरह लोग कर्ज के जाल में फंस जाते हैं।

The True Cost (Real APR) Calculator

असली लागत (Real APR) कैलकुलेटर

Don't trust the stated interest rate. Use the calculator below to input your loan details. It uses the standard Internal Rate of Return (IRR) formula to compute the Real Annualized Percentage Rate (APR) you are actually paying.

विज्ञापित ब्याज दर पर भरोसा न करें। अपने लोन की डिटेल्स डालने के लिए नीचे दिए गए कैलकुलेटर का उपयोग करें। यह आपको Real Annualized Percentage Rate (APR) बताने के लिए मानक Internal Rate of Return (IRR) फॉर्मूले का उपयोग करता है जो आप असल में चुका रहे हैं।

Reality Check

True Annualized Cost (Real APR)

The actual interest rate you are paying based on the money you received vs the EMI you pay (Standard IRR method).

Note: KreditBee advertises this specific 9-month loan at 48.89% APR. While the standard mathematical IRR calculates to ~42.7%, lending apps often use specific day-count conventions or constant ratio formulas that push the advertised APR even higher.

The "Credit Risk" Excuse: Busted

"क्रेडिट रिस्क" का बहाना: बेनकाब

If you ask these apps why their interest rates are so high, they will point you to their FAQ which says rates depend on "Credit Score, Income to Debt Ratio, Repayment History, etc." They claim that unsecured loans are highly risky, so they must charge 27%+ to cover potential defaults.

यदि आप इन ऐप्स से पूछें कि उनकी ब्याज दरें इतनी अधिक क्यों हैं, तो वे आपको अपने FAQ की ओर इशारा करेंगे जो कहता है कि दरें "क्रेडिट स्कोर, आय से ऋण अनुपात, पुनर्भुगतान इतिहास, आदि" पर निर्भर करती हैं। वे दावा करते हैं कि असुरक्षित ऋण अत्यधिक जोखिम भरे हैं, इसलिए संभावित डिफ़ॉल्ट को कवर करने के लिए उन्हें 27%+ शुल्क लेना होगा।

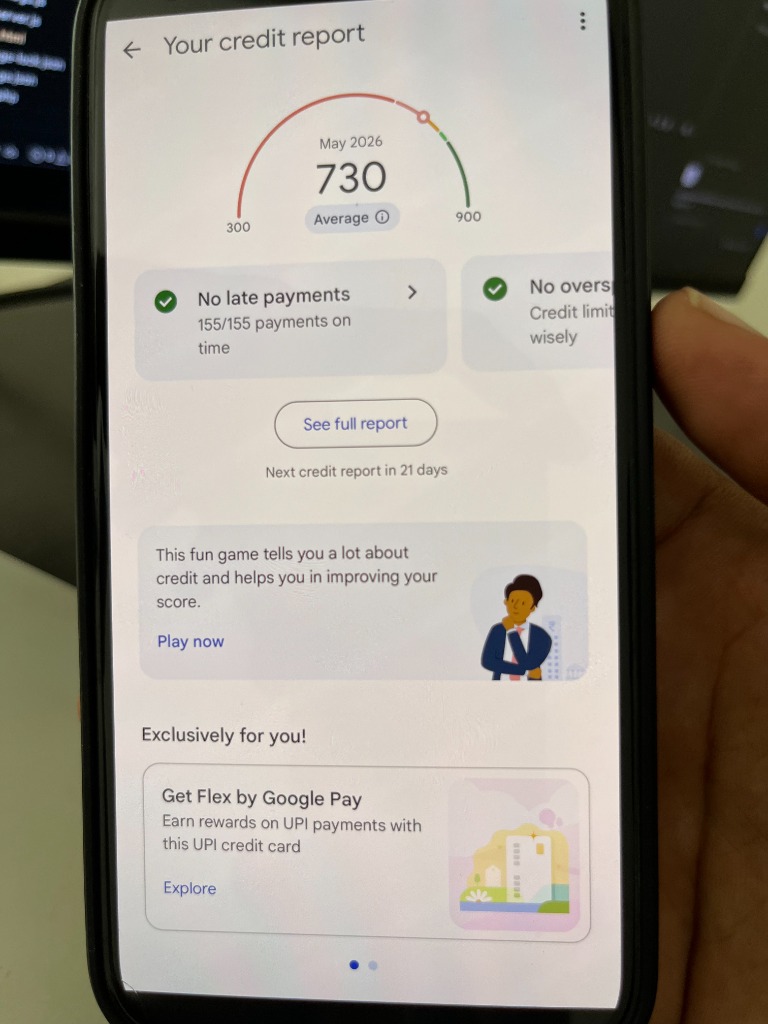

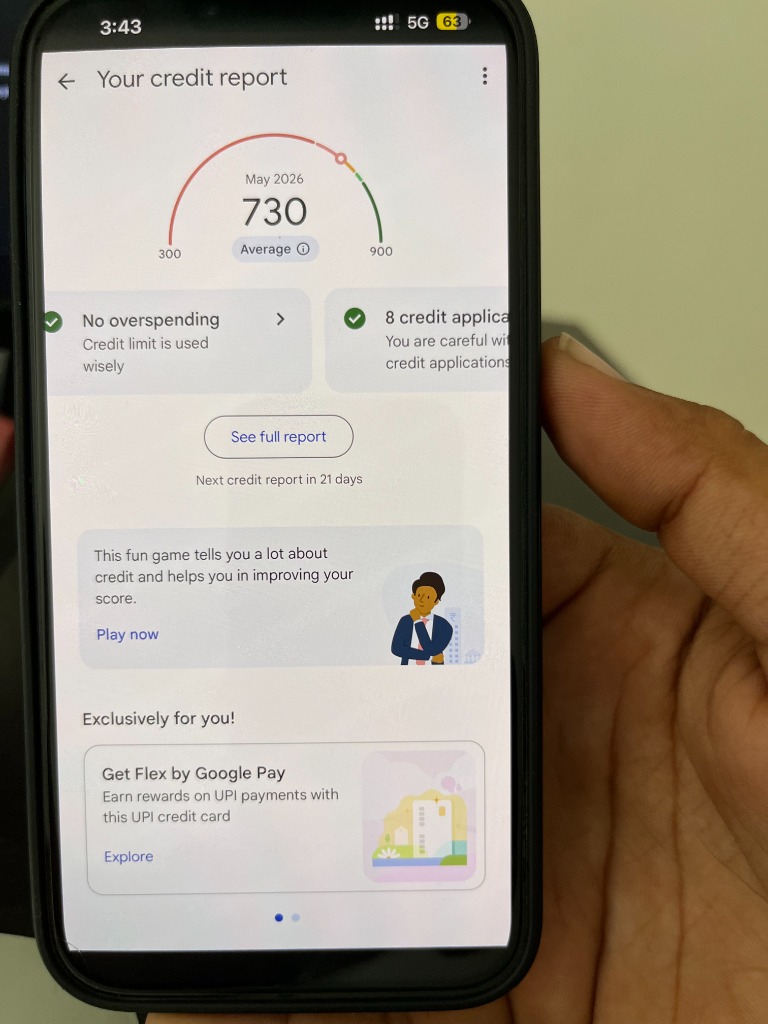

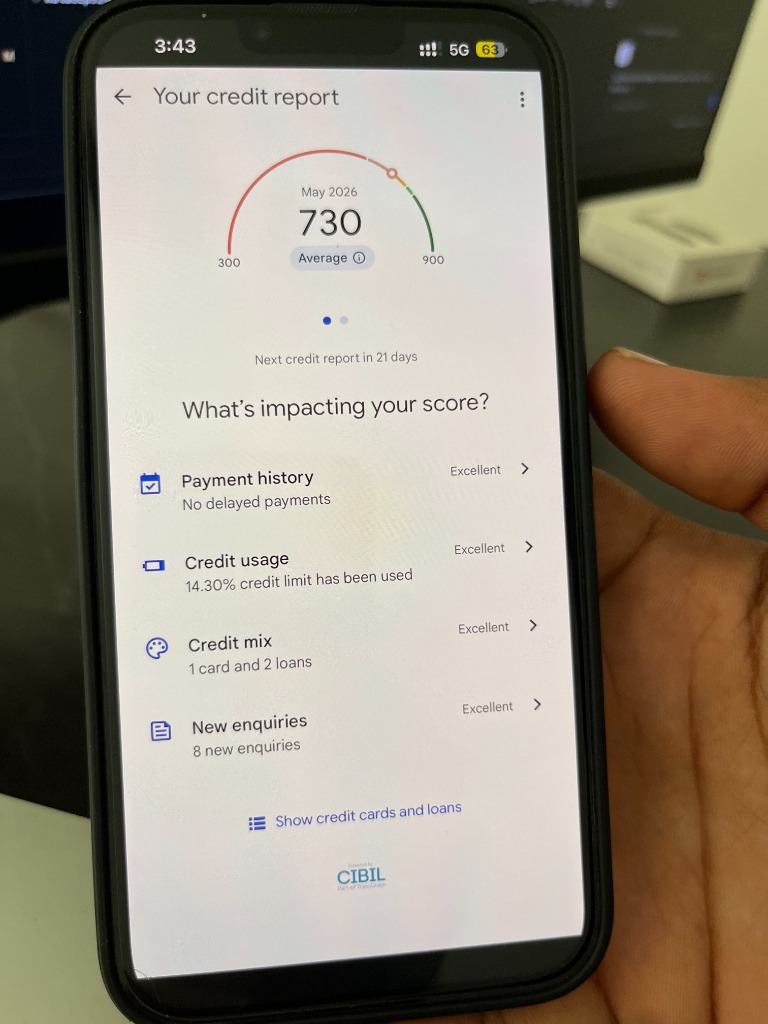

But is that really true? Let's look at my actual credit report from Google Pay (powered by CIBIL):

लेकिन क्या यह सच है? आइए Google Pay (CIBIL द्वारा संचालित) से मेरी असल क्रेडिट रिपोर्ट देखें:

As you can see, I have a solid 730 credit score. My payment history is flawless with 155 out of 155 payments on time, no overspending, and an "Excellent" rating across the board. Yet, despite having virtually zero default risk, the algorithm still slaps me with a 27.75% basic rate and a real APR of nearly 43% to 47%. The truth is, these platforms don't just charge high rates to cover risk; they charge high rates because they know people who need instant money are a captive audience.

जैसा कि आप देख सकते हैं, मेरा क्रेडिट स्कोर 730 है। मेरा पुनर्भुगतान इतिहास एकदम सही है, जिसमें 155 में से 155 भुगतान समय पर हुए हैं, कोई ओवरस्पेंडिंग नहीं है, और हर पैमाने पर "उत्कृष्ट" (Excellent) रेटिंग है। फिर भी, वस्तुतः शून्य डिफ़ॉल्ट जोखिम होने के बावजूद, एल्गोरिदम अभी भी मुझ पर 27.75% की मूल दर और लगभग 43% से 47% की असली APR लगाता है। सच्चाई यह है कि ये प्लेटफ़ॉर्म केवल जोखिम को कवर करने के लिए उच्च दरें नहीं लेते हैं; वे उच्च दरें वसूलते हैं क्योंकि वे जानते हैं कि जिन्हें तुरंत पैसे की आवश्यकता है उनकी कोई और मजबूरी नहीं है।

The Verdict

निष्कर्ष

Instant loan apps are highly convenient. They approve loans in minutes without tedious paperwork. But you pay a massive premium for that convenience.

इंस्टेंट लोन ऐप्स बहुत सुविधाजनक होते हैं। वे बिना किसी झंझट वाले कागजी काम के मिनटों में लोन पास कर देते हैं। लेकिन उस सुविधा के लिए आपको एक भारी कीमत चुकानी पड़ती है।

If you borrow ₹20,000 for 9 months and end up paying an effective rate of over 42%, you are trapping yourself in a cycle of expensive debt.

अगर आप 9 महीने के लिए ₹20,000 उधार लेते हैं और 42% से अधिक की प्रभावी दर चुकाते हैं, तो आप खुद को महंगे कर्ज के जाल में फंसा रहे हैं।

Always use our calculator to check the Real APR before accepting the offer. If the APR is above 15-18%, you should seriously reconsider taking the loan or look for traditional banking alternatives.

ऑफर स्वीकार करने से पहले हमेशा Real APR चेक करने के लिए हमारे कैलकुलेटर का उपयोग करें। यदि APR 15-18% से ऊपर है, तो आपको लोन लेने पर गंभीरता से पुनर्विचार करना चाहिए या पारंपरिक बैंकिंग विकल्पों की तलाश करनी चाहिए।

Frequently Asked Questions (FAQs)

अक्सर पूछे जाने वाले प्रश्न (FAQs)

1. Are there hidden charges in instant loan apps like KreditBee?

1. क्या KreditBee जैसे इंस्टेंट लोन ऐप में छिपे हुए शुल्क हैं?

▼

While they claim to be transparent, the "hidden" aspect is how they deduct a massive 5% to 6% processing fee + GST upfront from your principal. You pay EMI on the full amount, but you receive much less, pushing your real APR to 40%-50%.

हालाँकि वे पारदर्शी होने का दावा करते हैं, लेकिन "छिपा हुआ" पहलू यह है कि वे आपके मूलधन में से पहले ही 5% से 6% प्रोसेसिंग फीस + GST काट लेते हैं। आप पूरी राशि पर EMI देते हैं, लेकिन आपको बहुत कम मिलता है, जिससे आपकी असली APR 40%-50% हो जाती है।

2. What happens if I miss an EMI payment?

2. यदि मैं EMI का भुगतान करने से चूक जाऊं तो क्या होगा?

▼

This is where the debt trap begins. You will be hit with an immediate bounce charge of 4% of the overdue principal (or ₹500, whichever is lower), plus a brutal penal interest rate of 36% p.a. on the delayed amount.

यहीं से कर्ज का जाल शुरू होता है। आप पर तुरंत अतिदेय मूलधन का 4% बाउंस चार्ज (या ₹500, जो भी कम हो) लगाया जाएगा, साथ ही विलंबित राशि पर 36% p.a. की क्रूर दंडात्मक ब्याज दर लगाई जाएगी।

3. Can I close my loan early to save on interest?

3. क्या मैं ब्याज बचाने के लिए अपना लोन समय से पहले बंद कर सकता हूँ?

▼

Yes, but it will cost you. Foreclosure (paying off the loan early) usually attracts a penalty of 4% of the outstanding principal amount, plus 18% GST on that penalty charge.

हाँ, लेकिन इसमें भी आपका खर्च होगा। फोरक्लोज़र (लोन को समय से पहले चुकाने) पर आमतौर पर बकाया मूलधन का 4% जुर्माना लगता है, और उस जुर्माने पर 18% GST लगता है।

4. Will having a good credit score get me the 12% interest rate?

4. क्या अच्छा क्रेडिट स्कोर होने से मुझे 12% ब्याज दर मिलेगी?

▼

Almost never. As shown in our case study, even with a flawless 155/155 payment history and an Excellent credit profile, the basic interest rate offered was still 27.75%. The "12%" is mostly a marketing hook.

लगभग कभी नहीं। जैसा कि हमारे केस स्टडी में दिखाया गया है, 155/155 के त्रुटिहीन भुगतान इतिहास और उत्कृष्ट क्रेडिट प्रोफाइल के बावजूद, पेश की गई मूल ब्याज दर अभी भी 27.75% थी। "12%" ज्यादातर एक मार्केटिंग हुक है।

5. Can loan apps access my phone contacts or gallery?

5. क्या लोन ऐप मेरे फोन संपर्कों या गैलरी तक पहुंच सकते हैं?

▼

Yes, many apps ask for permission to your contacts and storage upon installation. If you default, many predatory and unregulated apps use these contacts to call your family and friends to harass them. Always check app permissions carefully.

हां, कई ऐप इंस्टॉलेशन के समय आपके संपर्कों और स्टोरेज की अनुमति मांगते हैं। यदि आप डिफ़ॉल्ट करते हैं, तो कई शिकारी और अनियमित ऐप आपके परिवार और दोस्तों को परेशान करने के लिए इन संपर्कों का उपयोग करते हैं। हमेशा ऐप अनुमतियों की सावधानीपूर्वक जांच करें।

6. Is it legal for recovery agents to harass me or call my relatives?

6. क्या रिकवरी एजेंटों के लिए मुझे परेशान करना या मेरे रिश्तेदारों को कॉल करना कानूनी है?

▼

Absolutely not. According to strict RBI guidelines, harassment, abusive language, or calling relatives is illegal. If this happens, you can and should file a complaint with the RBI Ombudsman or the cybercrime portal.

बिल्कुल नहीं। सख्त RBI दिशानिर्देशों के अनुसार, उत्पीड़न, अपमानजनक भाषा, या रिश्तेदारों को फोन करना अवैध है। यदि ऐसा होता है, तो आप RBI लोकपाल या साइबर अपराध पोर्टल पर शिकायत दर्ज कर सकते हैं और करनी चाहिए।

7. What happens if a loan app sends me a legal notice on WhatsApp?

7. क्या होगा यदि कोई लोन ऐप मुझे व्हाट्सएप पर कानूनी नोटिस भेजता है?

▼

Unregulated apps often send fake police complaints or bogus legal notices via WhatsApp to scare you into paying. A genuine legal notice is sent via registered post or official channels, not through a random WhatsApp message.

अनियमित ऐप अक्सर आपको डराकर भुगतान कराने के लिए व्हाट्सएप के माध्यम से फर्जी पुलिस शिकायतें या फर्जी कानूनी नोटिस भेजते हैं। एक वास्तविक कानूनी नोटिस पंजीकृत डाक या आधिकारिक चैनलों के माध्यम से भेजा जाता है, न कि किसी व्हाट्सएप संदेश के माध्यम से।

8. Can I be arrested for defaulting on an instant loan?

8. क्या इंस्टेंट लोन चुकाने में विफल रहने पर मुझे गिरफ्तार किया जा सकता है?

▼

No. Defaulting on a personal loan is a civil dispute, not a criminal offense. You cannot be sent to jail simply for missing EMI payments. Do not fall for these scare tactics.

नहीं। व्यक्तिगत ऋण पर डिफ़ॉल्ट करना एक नागरिक विवाद है, आपराधिक अपराध नहीं। केवल EMI भुगतान से चूकने के कारण आपको जेल नहीं भेजा जा सकता है। इन डराने वाली चालों में न पड़ें।

9. Do these loan apps report defaults to CIBIL?

9. क्या ये लोन ऐप CIBIL को डिफ़ॉल्ट रिपोर्ट करते हैं?

▼

Legitimate, RBI-registered NBFCs (like the ones partnered with KreditBee) absolutely do report to credit bureaus like CIBIL. A default will severely impact your credit score, making it difficult to get loans for up to 7 years.

वैध, RBI-पंजीकृत NBFC (जैसे कि KreditBee के साथ भागीदार) बिल्कुल CIBIL जैसे क्रेडिट ब्यूरो को रिपोर्ट करते हैं। डिफ़ॉल्ट आपके क्रेडिट स्कोर को गंभीर रूप से प्रभावित करेगा, जिससे 7 वर्षों तक ऋण प्राप्त करना मुश्किल हो जाएगा।

10. Why did my disbursed loan amount not match the approved amount?

10. मेरी वितरित ऋण राशि स्वीकृत राशि से मेल क्यों नहीं खाती?

▼

Loan apps deduct the processing fee and GST upfront before sending money to your bank account. If you are approved for ₹20,000 and the processing fee is 5%, you will receive around ₹18,800 but will still be charged interest on the full ₹20,000.

लोन ऐप आपके बैंक खाते में पैसे भेजने से पहले प्रोसेसिंग फीस और GST काट लेते हैं। यदि आपको ₹20,000 स्वीकृत किए गए हैं और प्रोसेसिंग फीस 5% है, तो आपको लगभग ₹18,800 प्राप्त होंगे लेकिन फिर भी आपसे पूरे ₹20,000 पर ब्याज लिया जाएगा।