The "Free Money" Trap of Mutual Funds

म्यूचुअल फंड का "फ्री मनी" ट्रैप

Let's get one thing straight about mutual funds right now, otherwise, you are going to get played terribly in the long run. If you started investing around 2015 or later, you've probably heard the term "Dividend Mutual Funds."

म्यूचुअल फंड्स के बारे में एक बात अभी क्लियर कर लो, वरना लॉन्ग टर्म में आपका तगड़ा पोपट होने वाला है। अगर आपने 2015 या उसके बाद इन्वेस्ट करना स्टार्ट किया है, तो आपने पक्का "डिविडेंड म्यूचुअल फंड्स" के बारे में सुना होगा।

"Bro, my capital is growing AND I'm getting free cash! Double win! 🤑"

"भाई, मेरी कैपिटल भी ग्रो कर रही है और मुझे फ्री कैश भी मिल रहा है! डबल मज़े! 🤑"

It feels amazing. You think the mutual fund company is happy enough to hand you some extra "bonus" cash on top of your market returns. But it doesn't work like that. This "free money" dream was a complete illusion.

ये सुनने में बहुत मस्त लगता है। आपको लगता है कि म्यूचुअल फंड कंपनी आपके मार्केट रिटर्न के ऊपर कुछ एक्स्ट्रा "बोनस" कैश देने में बड़ी खुश है। लेकिन असल में ऐसा कुछ नहीं होता। यह "फ्री मनी" वाला सपना पूरी तरह से एक इल्यूजन (धोखा) था।

🛑 SEBI Entered the Chat (2020)

🛑 SEBI की धाकड़ एंट्री (2020)

Mutual fund companies milked the word "Dividend" to trick the public. People were investing blindly, thinking they were getting free money. Then in 2020, SEBI stepped in and said: "Stop right there!" ✋

म्यूचुअल फंड कंपनियों ने पब्लिक को बेवकूफ बनाने के लिए "डिविडेंड" शब्द का जमकर फायदा उठाया। लोग आँख बंद करके इन्वेस्ट कर रहे थे, ये सोचकर कि उन्हें फ्री का पैसा मिल रहा है। फिर 2020 में, SEBI ने एंट्री ली और बोला: "बस, बहुत हो गया!" ✋

SEBI passed a strict rule banning all mutual funds from ever using the word "Dividend" in their plans again. They forced them to change the name to a confusing acronym: IDCW.

SEBI ने एक स्ट्रिक्ट रूल पास किया और सारे म्यूचुअल फंड्स को अपने प्लान्स में "डिविडेंड" वर्ड यूज़ करने से बैन कर दिया। उन्होंने कंपनीज़ को इसका नाम बदलकर एक कन्फ्यूज़िंग शॉर्ट फॉर्म रखने पर फोर्स किया: IDCW.

The Truthसच्चाई

🤔 What the Hell is IDCW?

🤔 IDCW क्या बला है?

IDCW stands for Income Distribution cum Capital Withdrawal. Look closely at those last two words: Capital Withdrawal.

IDCW का फुल फॉर्म है इनकम डिस्ट्रीब्यूशन कम कैपिटल विथड्रॉल। इसके लास्ट दो वर्ड्स को ध्यान से देखो: कैपिटल विथड्रॉल (यानी अपनी ही इन्वेस्टेड कैपिटल को वापस निकालना)।

The Brutal Reality Checkब्रूटल रियलिटी चेक

This is what the mutual fund companies were hiding from you. When a mutual fund gave you a "dividend," they weren't gifting you extra profits from their own pockets. They were literally taking a piece of your own invested capital and handing it back to you!

यही बात म्यूचुअल फंड कंपनीज़ आपसे छुपा रही थीं। जब कोई म्यूचुअल फंड आपको "डिविडेंड" दे रहा था, तो वो अपनी जेब से कोई एक्स्ट्रा प्रॉफिट गिफ्ट नहीं कर रहा था। वो लिटरली आपके ही इन्वेस्ट किए हुए पैसे का एक हिस्सा निकाल कर आपको वापस थमा रहे थे!

The Piggy Bank Example 🐷

पिग्गी बैंक वाला एग्जांपल 🐷

Imagine your mutual fund is a piggy bank with ₹100 in it. The company announces: "We are giving a ₹5 dividend!" You get excited! 🎉 But what did they actually do? They took ₹5 out of your piggy bank and put it in your hand. Now your piggy bank only has ₹95 left. No new money was magically generated; you just pulled money out of your own pocket.

इमेजिन करो कि आपका म्यूचुअल फंड एक पिग्गी बैंक (गुल्लक) है जिसमें ₹100 रखे हैं। कंपनी अनाउंस करती है: "हम ₹5 का डिविडेंड दे रहे हैं!" आप एक्साइटेड हो जाते हो! 🎉 लेकिन उन्होंने असल में किया क्या? उन्होंने आपके गुल्लक से ही ₹5 निकाले और आपके हाथ में रख दिए। अब आपके गुल्लक में सिर्फ ₹95 बचे हैं। कोई नया पैसा मैजिक से जनरेट नहीं हुआ; आपने बस अपनी ही जेब से पैसा निकाल लिया।

📉 The Ultimate Proof: Where Did My 10% Go?

📉 अल्टीमेट प्रूफ: मेरा 10% कहाँ गया?

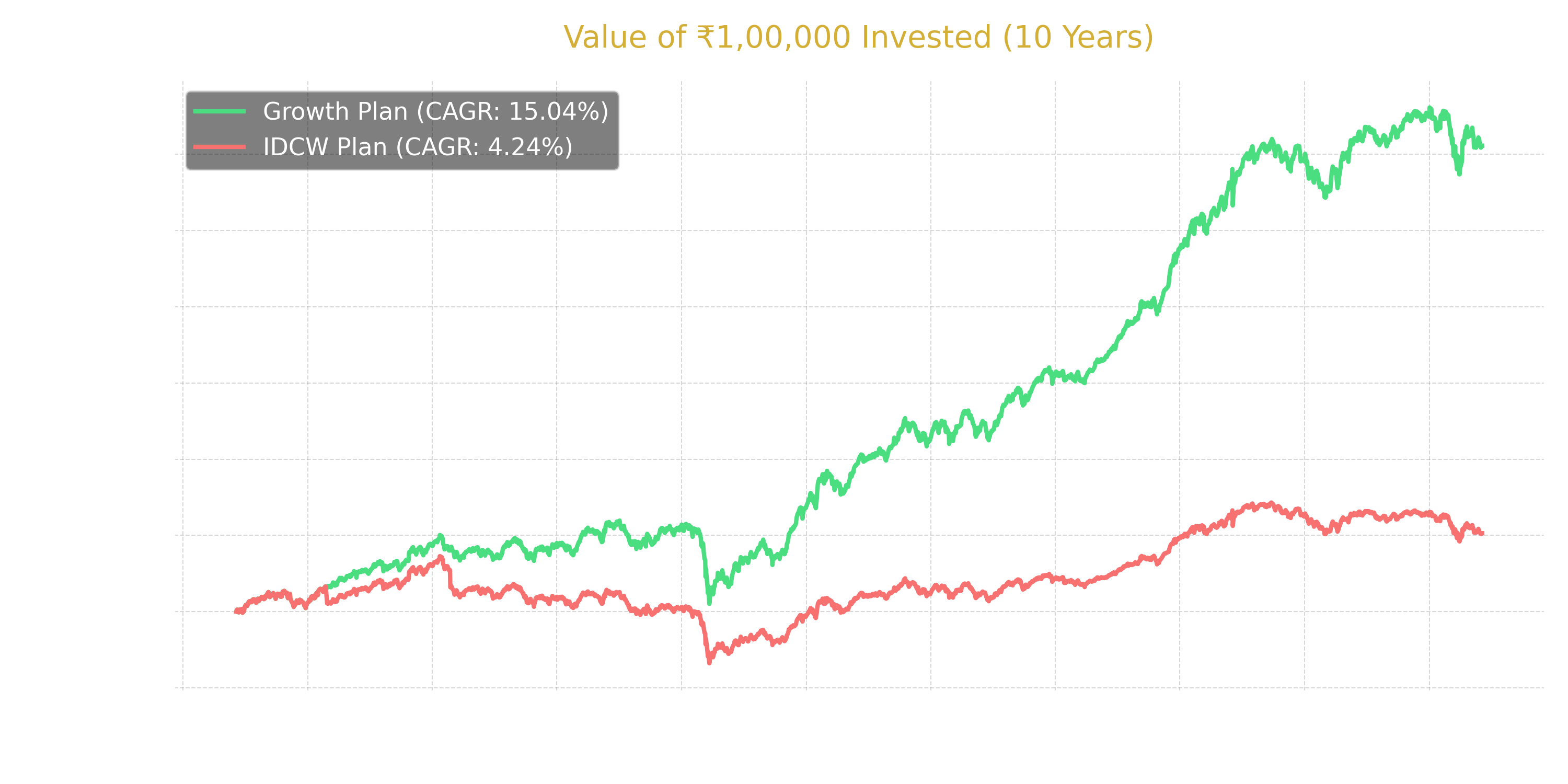

If you are thinking, "Whatever, it's still my money," look at this real-world example. It will blow your mind. Let's take the famous HDFC Balanced Advantage Fund. If we look at the 10-year returns (XIRR) of its two identical plans side-by-side:

अगर आप सोच रहे हो, "छोड़ो यार, है तो मेरा ही पैसा", तो इस रियल-वर्ल्ड एग्जांपल को देखो। आपका दिमाग हिल जाएगा। चलिए फेमस HDFC बैलेंस्ड एडवांटेज फंड को देखते हैं। अगर हम इसके दो एकदम सेम प्लान्स के 10-साल के रिटर्न (XIRR) को साइड-बाय-साइड रखकर देखें:

*Data used from 06 Jun 2016 to 05 Jun 2026

*डेटा 06 जून 2016 से 05 जून 2026 तक का है

🚀 Direct Growth Plan🚀 डायरेक्ट ग्रोथ प्लान

~15.04% CAGR

🐢 IDCW Plan🐢 IDCW प्लान

~4.24% CAGR

Both funds are exactly the same. Same manager, same stocks. So where did that missing 10%+ return go? That money didn't sink in the stock market. That money was repeatedly scooped out of your mutual fund under the name of "dividends" and dumped into your bank account. Because cash kept leaving the bucket, your money never actually got the chance to compound properly!

दोनों फंड्स एकदम सेम हैं। सेम मैनेजर, सेम स्टॉक्स। तो वो 10%+ रिटर्न कहाँ गायब हो गया? वो पैसा शेयर मार्केट में नहीं डूबा। उस पैसे को "डिविडेंड" के नाम पर आपके म्यूचुअल फंड से बार-बार निकाला गया और सीधा आपके बैंक अकाउंट में डंप कर दिया गया। क्योंकि पैसा लगातार बकेट से बाहर जा रहा था, इसलिए आपके पैसे को कभी भी प्रॉपर तरीके से कंपाउंड होने का मौका ही नहीं मिला!

💸 The Tax Trap: Rubbing Salt in the Wound

💸 टैक्स का जाल: जले पर नमक छिड़कना

Wait, the worst part is still left. This is where you truly get played. In a Growth plan, all your profit is automatically reinvested into the fund and quietly compounds. It is completely tax-free until you finally decide to sell years later.

रुको, वर्स्ट पार्ट तो अभी बाकी है। यहीं पर आपके साथ असली गेम होता है। ग्रोथ प्लान में, आपका सारा प्रॉफिट अपने-आप फंड में वापस री-इन्वेस्ट हो जाता है और चुपचाप कंपाउंड होता रहता है। ये पूरी तरह से टैक्स-फ्री है, तब तक, जब तक कि आप सालों बाद फाइनली इसे सेल करने का डिसीज़न नहीं लेते।

But in IDCW? Every time that so-called "dividend" hits your bank account, the Tax Department is standing outside waiting to say, "Welcome, bro!"

लेकिन IDCW में? हर बार जब वो सो-कॉल्ड "डिविडेंड" आपके बैंक अकाउंट में हिट करता है, तो इनकम टैक्स वाले बाहर खड़े आपका वेट कर रहे होते हैं ये कहने के लिए, "आइए बॉस!"

You have to pay a flat tax on every single dividend payout according to your income slab. So, you are withdrawing your own money, killing your own compound interest, AND paying taxes on it immediately. A literal masterstroke of getting played! 🤡

आपको अपने इनकम स्लैब के अकॉर्डिंग हर सिंगल डिविडेंड पेआउट पर फ्लैट टैक्स पे करना पड़ता है। मतलब, आप अपना ही पैसा निकाल रहे हो, अपने खुद के कंपाउंड इंटरेस्ट का मर्डर कर रहे हो, और उस पर इमीडिएटली टैक्स भी भर रहे हो। लिटरली बेवकूफ बनने का एक मास्टरस्ट्रोक! 🤡

💡 The Bottom Line

💡 असली ज्ञान

If you want to build long-term wealth and actually see the magic of compounding, do not fall for these fancy terms. Stay far away from IDCW. Whenever you buy a mutual fund, blindly select the "Growth" option. Let your money grow peacefully in the market, and don't disturb it in between. Keep it simple, let it compound, and you won't get played!

अगर आप लॉन्ग-टर्म वेल्थ बिल्ड करना चाहते हो और सच में कंपाउंडिंग का मैजिक देखना चाहते हो, तो इन फैंसी वर्ड्स के ट्रैप में बिलकुल मत फंसना। IDCW से कोसों दूर रहो। जब भी कोई म्यूचुअल फंड खरीदो, तो आँख बंद करके "ग्रोथ" ऑप्शन सेलेक्ट कर लेना। अपने पैसे को पीसफुली मार्केट में ग्रो होने दो, और बीच में उसे उंगली मत करो। एकदम सिंपल रखो, इसे कंपाउंड होने दो, और आपका कभी पोपट नहीं बनेगा!

Frequently Asked Questions (FAQs)

अक्सर पूछे जाने वाले प्रश्न (FAQs)

1. If IDCW is such a trap, why do mutual fund companies even offer it?

1. अगर IDCW इतना बड़ा ट्रैप है, तो म्यूचुअल फंड कंपनीज़ इसे ऑफर ही क्यों करती हैं?

▼

Because it sells! People are emotionally attached to the idea of "passive income" and getting a regular payout. It is a psychological marketing tactic to attract investors who want to see cash hitting their accounts, even if it is mathematically a terrible idea for building actual wealth.

क्योंकि ये बिकता है! लोग "पैसिव इनकम" और रेगुलर पेआउट के आइडिया से इमोशनली अटैच होते हैं। ये इन्वेस्टर्स को अट्रैक्ट करने की एक साइकोलॉजिकल मार्केटिंग टैक्टिक है, जिन्हें अपने अकाउंट में कैश आते देखना पसंद है, भले ही वेल्थ क्रिएट करने के लिए मैथमेटिकली ये एक बहुत ही बकवास आइडिया हो।

2. But what if I am retired and actually need a regular monthly income?

2. लेकिन क्या हो अगर मैं रिटायर्ड हूँ और मुझे सच में रेगुलर मंथली इनकम चाहिए?

▼

Then use an SWP (Systematic Withdrawal Plan) on a Growth fund! With an SWP, you are in the driver's seat. You decide exactly how much money you want to withdraw every month, not the fund manager. Plus, an SWP is incredibly tax-efficient compared to the brutal flat taxation of IDCW payouts.

तो फिर ग्रोथ फंड पर SWP (सिस्टमैटिक विथड्रॉल प्लान) यूज़ करो ना! SWP में कंट्रोल आपके हाथ में होता है। आप खुद डिसाइड करते हो कि हर महीने आपको कितना पैसा निकालना है, न कि फंड मैनेजर। इसके अलावा, IDCW पेआउट्स के ब्रूटल फ्लैट टैक्स के कंपैरिजन में SWP बहुत ही ज्यादा टैक्स-एफिशिएंट है।

3. Wait, so that 10% difference in returns you showed... did it just vanish into thin air?

3. रुको, तो वो जो 10% रिटर्न्स का डिफरेंस आपने दिखाया... क्या वो हवा में गायब हो गया?

▼

Nope! The mutual fund didn't steal it. That missing 10% is simply the cash that was forcefully evicted from your compounding machine and dumped into your savings account over the last decade. But if you spent those payouts on new phones or trips instead of reinvesting them... then yeah, that wealth is gone forever!

नहीं! म्यूचुअल फंड ने उसे चुराया नहीं है। वो मिसिंग 10% बस वो कैश है जिसे पिछले 10 सालों में आपकी कंपाउंडिंग मशीन से ज़बरदस्ती बाहर निकाल कर आपके सेविंग्स अकाउंट में डंप कर दिया गया। लेकिन अगर आपने वो पैसा री-इन्वेस्ट करने की बजाय नए फोन या ट्रिप्स पर खर्च कर दिया... तो हाँ, वो वेल्थ हमेशा के लिए गायब हो गई!

4. What if I choose the "IDCW Reinvestment" option? Does that fix the problem?

4. क्या होगा अगर मैं "IDCW Reinvestment" ऑप्शन चुन लूं? क्या इससे प्रॉब्लम फिक्स हो जाएगी?

▼

NO! And this is the biggest joke of all. Even if you tell the mutual fund to automatically reinvest your payout to buy more units, the tax department still treats it as "income received." You will literally pay taxes on money that never even reached your hands. Do not overcomplicate your life—just stick to pure Growth.

बिलकुल नहीं! और ये तो सबसे बड़ा जोक है। अगर आप म्यूचुअल फंड से कहते हो कि वो आपके पेआउट को ऑटोमैटिकली नई यूनिट्स खरीदने के लिए री-इन्वेस्ट कर दे, तब भी इनकम टैक्स डिपार्टमेंट इसे "इनकम रिसीव्ड" ही मानता है। आप लिटरली उस पैसे पर टैक्स दोगे जो आपके हाथों तक पहुँचा ही नहीं। अपनी लाइफ को ओवर-कॉम्प्लिकेट मत करो—बस प्योर ग्रोथ ऑप्शन से चिपके रहो।

5. Is the IDCW payout amount guaranteed every month or year?

5. क्या IDCW का पेआउट अमाउंट हर महीने या साल गारंटीड होता है?

▼

Not at all. The mutual fund manager decides if they want to pay out, when they want to pay out, and how much. If the market is crashing, they might just stop paying altogether. Relying on IDCW for a fixed monthly income is a massive mistake.

बिलकुल नहीं। म्यूचुअल फंड मैनेजर ये डिसाइड करता है कि उन्हें पेआउट देना है या नहीं, कब देना है, और कितना देना है। अगर मार्केट क्रैश हो रहा है, तो हो सकता है वो पेआउट देना ही बंद कर दें। फिक्स्ड मंथली इनकम के लिए IDCW पर रिलाई करना एक बहुत बड़ी गलती है।

6. I didn't know this and I already bought an IDCW fund. What should I do now?

6. मुझे ये नहीं पता था और मैं पहले ही एक IDCW फंड ले चुका हूँ। अब मुझे क्या करना चाहिए?

▼

Don't panic, but fix it. You can place a "Switch" request on your broker app to move your money from the IDCW plan to the Direct Growth plan of the exact same fund. Just keep an eye on exit loads (usually 1% if you sell before a year) and standard capital gains taxes when making the switch.

पैनिक मत करो, बस इसे फिक्स कर लो। आप अपने ब्रोकर ऐप पर उसी फंड के IDCW प्लान से डायरेक्ट ग्रोथ प्लान में पैसा मूव करने के लिए एक "Switch" रिक्वेस्ट डाल सकते हो। बस स्विच करते टाइम एग्जिट लोड (यूज़ुअली 1% अगर आप एक साल से पहले बेचते हो) और स्टैंडर्ड कैपिटल गेन्स टैक्स का ध्यान रखना।

7. Doesn't IDCW work like stock dividends?

7. क्या IDCW स्टॉक्स के डिविडेंड की तरह काम नहीं करता?

▼

No, and this is why SEBI banned the word! When a company like ITC or Reliance pays a stock dividend, they are sharing their corporate profits. When a mutual fund pays an IDCW, they are literally selling a tiny fraction of your mutual fund units to give you cash. You are just eating your own capital.

नहीं, और इसीलिए SEBI ने इस वर्ड को बैन किया था! जब ITC या Reliance जैसी कंपनी स्टॉक डिविडेंड देती है, तो वो अपना कॉर्पोरेट प्रॉफिट शेयर कर रही होती है। पर जब कोई म्यूचुअल फंड IDCW पे करता है, तो वो लिटरली आपको कैश देने के लिए आपकी ही म्यूचुअल फंड यूनिट्स का एक छोटा सा हिस्सा सेल कर रहे होते हैं। आप बस अपनी ही कैपिटल खा रहे हो।

8. Does the NAV always drop exactly by the payout amount?

8. क्या NAV हमेशा पेआउट अमाउंट के बराबर ही गिरती है?

▼

Yes. 100% of the time. It is pure math. If the NAV is ₹100 and they declare a ₹5 payout, the NAV instantly drops to ₹95. There is no magic formula—money left the mutual fund bucket, so the bucket is now worth less.

हाँ। 100% हमेशा। ये प्योर मैथ्स है। अगर NAV ₹100 है और वो ₹5 का पेआउट डिक्लेयर करते हैं, तो NAV इंस्टेंटली गिरकर ₹95 हो जाती है। इसमें कोई मैजिक फॉर्मूला नहीं है—म्यूचुअल फंड की बकेट से पैसा बाहर निकला, तो अब उस बकेट की वैल्यू कम हो गई।

9. Can I use IDCW funds to build long-term generational wealth?

9. क्या मैं लॉन्ग-टर्म जनरेशनल वेल्थ बिल्ड करने के लिए IDCW फंड्स यूज़ कर सकता हूँ?

▼

Absolutely not. Building generational wealth requires the eighth wonder of the world: Compound Interest. IDCW acts like a pair of scissors, constantly cutting your compound interest before it gets a chance to grow massive.

बिलकुल नहीं। जनरेशनल वेल्थ बिल्ड करने के लिए दुनिया के आठवें अजूबे की जरूरत होती है: कंपाउंड इंटरेस्ट। IDCW कैंची की तरह काम करता है, जो आपके कंपाउंड इंटरेस्ट को मैसिव होने से पहले ही लगातार काटता रहता है।

10. How can I check if my current mutual funds are Growth or IDCW?

10. मैं ये कैसे चेक कर सकता हूँ कि मेरे करेंट म्यूचुअल फंड्स ग्रोथ हैं या IDCW?

▼

Open your broker app (Groww, Zerodha, Upstox, etc.) or check your NSDL/CDSL statement. Look at the full, exact name of your fund. If you see the words "IDCW" or "Payout" or "Reinvestment" at the end of the name, you are in the trap. If it says "Direct Plan - Growth", you are completely safe! (You can also run your fund's name through the Deep Money Minds backtester to see the visual proof of what you might be losing!)

अपना ब्रोकर ऐप (Groww, Zerodha, Upstox, वगैरह) ओपन करो या अपना NSDL/CDSL स्टेटमेंट चेक करो। अपने फंड का पूरा एग्ज़ैक्ट नाम देखो। अगर आपको नाम के एंड में "IDCW", "Payout" या "Reinvestment" वर्ड्स दिखें, तो आप ट्रैप में हो। अगर ये "Direct Plan - Growth" कहता है, तो आप पूरी तरह से सेफ हो! (आप अपनी तसल्ली के लिए Deep Money Minds बैकटेस्टर में भी अपने फंड का नाम डाल कर विजुअल प्रूफ देख सकते हो कि आप कितना लूज़ कर रहे होंगे!)