The FoF Trap: How Paying for 'Convenience' is Emptying Your WalletFoF का जाल: कैसे "सुविधा" के नाम पर आपका पैसा कट रहा है

So, you open your favorite shiny investing app, click 'Invest' on something that looks super easy, and think you're a genius. Congrats! You just walked right into a trap called a Fund of Funds (FoF). Yeah, that 'convenience' is costing you big time.तो, आप अपना फेवरेट इन्वेस्टिंग ऐप खोलते हैं, एक मस्त से दिखने वाले ऑप्शन पर 'इन्वेस्ट' क्लिक करते हैं और खुद को जीनियस समझते हैं। बधाई हो! आप फंड ऑफ फंड्स (FoF) नाम के जाल में फंस चुके हैं। जी हां, ये 'सुविधा' आपको बहुत महंगी पड़ रही है।

They sell you this beautiful story: 'Hey, just give us your money, we'll pick the best funds for you! It's so diversified!' Sounds great, right? In reality, it's just a sneaky excuse to charge you double fees while you sleep.वो आपको एक बढ़िया कहानी सुनाते हैं: 'बस अपना पैसा हमें दे दो, हम आपके लिए बेस्ट फंड्स चुनेंगे!' सुनने में मस्त लगता है ना? असल में, ये बस सोते हुए आपसे डबल फीस वसूलने का एक बहाना है।

Let me show you how the industry hides this little secret. If you keep buying these FoFs blindly—especially the 'Regular' ones—you're basically donating your retirement money to someone else.चलिए मैं दिखाता हूं कि ये इंडस्ट्री अपना ये छोटा सा राज कैसे छुपाती है। अगर आप आंख बंद करके ये FoFs खरीदते रहे—खासकर 'रेगुलर' वाले—तो समझो आप अपना पैसा किसी और को दान कर रहे हैं।

1. The Double (and Triple) Fee Joke1. डबल फीस वाला घोटाला

Look, when you buy a normal mutual fund, you pay a small fee. That's fair. But when you buy a Fund of Funds, you don't just pay one fee. Oh no, you pay a hidden stack of fees!देखो यार, जब आप एक नॉर्मल म्यूचुअल फंड खरीदते हो, तो आप एक छोटी सी फीस देते हो। वो तो ठीक है। लेकिन जब आप एक फंड ऑफ फंड्स खरीदते हो, तो आप सिर्फ एक फीस नहीं देते। आप कई सारी छिपी हुई फीस दे रहे होते हो!

Layer 1: You pay a fee for the main FoF you just bought.लेयर 1: आप उस मेन FoF की फीस देते हो जिसे आपने अभी खरीदा है।

Layer 2: You ALSO pay the fees of every single fund hiding inside that FoF. Surprise!लेयर 2: आप उन सभी फंड्स की भी फीस देते हो जो उस FoF के अंदर छिपे हुए हैं। सरप्राइज़!

So if the main fund charges 0.5% and the hidden funds charge 1.0%, you're throwing away 1.5% of your money every single year. Over 15 to 20 years, this joke will literally wipe out lakhs of rupees from your savings. Thanks for playing!तो अगर मेन फंड 0.5% चार्ज करता है और अंदर छिपे फंड्स 1.0% लेते हैं, तो आप हर साल अपना 1.5% पैसा पानी में बहा रहे हो। 15-20 सालों में, ये मज़ाक आपके लाखों रुपये साफ कर देगा।

2. Real Example: The Gold Fund Trick2. असली उदाहरण: गोल्ड फंड का खेल

Let’s look at a real example of how silly this gets. Let's take something simple like a Gold Fund.आइए एक असली उदाहरण से समझते हैं कि ये कितना बेवकूफी भरा है। एक सिंपल से गोल्ड फंड को ही ले लो।

What it actually doesये असल में करता क्या है

It doesn’t buy real gold. It doesn't do any smart research. It literally just takes your money, walks across the room, and buys a Gold ETF. It’s just an expensive wrapper.ये असली सोना नहीं खरीदता। ये कोई तगड़ी रिसर्च भी नहीं करता। ये बस आपका पैसा लेता है और जाकर गोल्ड ईटीएफ (Gold ETF) खरीद लेता है। ये बस एक महंगा डब्बा है।

The Price of 'Convenience'"सुविधा" की कीमत

If you just buy a Gold ETF directly, you pay a tiny fee. But if you buy the Gold 'Mutual Fund', you pay an extra premium just because you were too lazy to open a demat account. Good job!अगर आप सीधे एक गोल्ड ईटीएफ खरीद लो, तो फीस बहुत कम लगती है। लेकिन अगर आप गोल्ड 'म्यूचुअल फंड' खरीदते हो, तो आप बस इसलिए एक्स्ट्रा पैसा दे रहे हो क्योंकि आपको डीमैट अकाउंट खोलने में आलस आ रहा था। बढ़िया काम किया!

3. The 'Regular Plan' Trap3. "रेगुलर प्लान" का असली ट्रैप

Oh, but wait, it gets worse! If you go to easy-to-use apps like PhonePe and click buy, they sneakily put you in a 'Regular Plan'. Let's do the math on how badly you're getting played here:अरे रुको, अभी तो पिक्चर बाकी है! अगर आप PhonePe जैसे ऐप्स पर जाकर बाय (buy) करते हो, तो वो चुपके से आपको 'रेगुलर प्लान' थमा देते हैं। चलिए देखते हैं कि कैसे आपका पोपट बन रहा है:

Who You Are Payingआप किसे पैसे दे रहे हो

Rough Costलगभग खर्चा

The Hidden Fund's Feeछिपे हुए फंड की फीस

~0.35%

The Main Fund's Feeमेन फंड की फीस

~0.15%

The App's Commission (Just for showing you a button)ऐप का कमीशन (बस एक बटन दिखाने का)

Extra ~0.40% to 0.50%

Total Money Lostटोटल पैसा डूबा

Close to 1% or more!लगभग 1% या उससे ज्यादा!

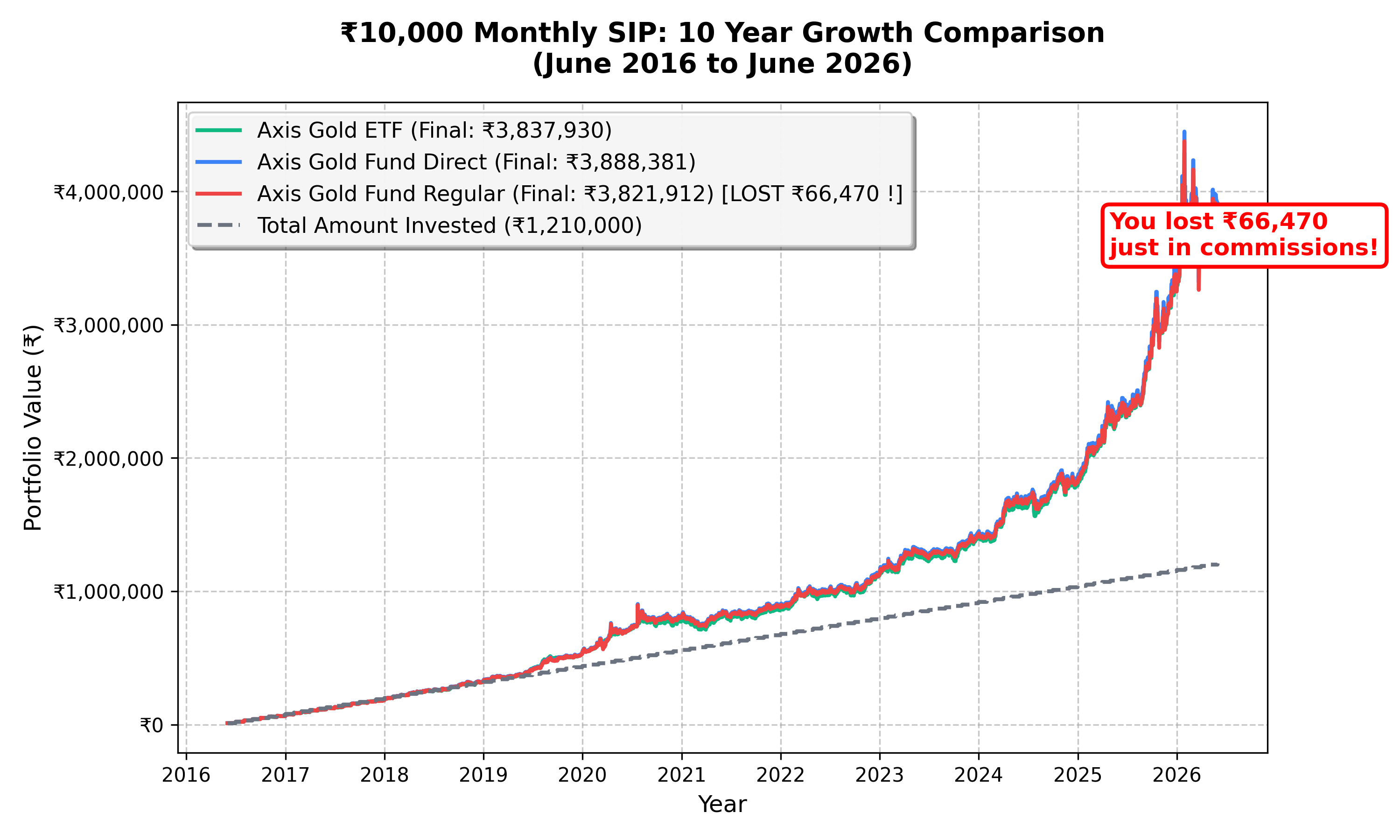

Don't believe me? Let's look at the actual historical data. We simulated a ₹10,000 monthly SIP from June 2016 to June 2026 across Axis Gold ETF, Axis Gold Fund Direct, and Axis Gold Fund Regular. The results are shocking. Over 10 years, just by choosing the "Regular" plan, you lost over ₹66,469 in pure commissions for absolutely zero extra benefit. Here is the visual proof:मुझ पर विश्वास नहीं है? चलिए असली डेटा देखते हैं। हमने जून 2016 से 2026 तक 10,000 रुपये की SIP को टेस्ट किया। नतीजे देखकर दिमाग खराब हो जाएगा। 10 सालों में, बस "रेगुलर" प्लान चुनने की वजह से, आपने ₹66,469 सिर्फ कमीशन में उड़ा दिए और फायदा जीरो मिला। ये रहा सबूत:

So, just to track the price of gold—which requires zero brainpower from a fund manager—you're losing around 1% of your money every year. You are paying three different people to do a job you could have done yourself with two clicks.तो, बस सोने के दाम को ट्रैक करने के लिए—जिसमें फंड मैनेजर का कोई दिमाग नहीं लगता—आप हर साल अपना 1% पैसा गँवा रहे हो। आप तीन अलग-अलग लोगों को वो काम करने के पैसे दे रहे हो जो आप खुद दो क्लिक में कर सकते थे।

4. Why Regular FoFs Are Terrible For You4. रेगुलर FoF आपके लिए इतने बुरे क्यों हैं

If you buy a Regular FoF, you're paying an app a lifetime commission to hand your money to a guy, who then hands your money to another guy. Everyone takes a slice of your pie. By the time the returns reach you, there's barely any pie left.अगर आप रेगुलर FoF खरीदते हो, तो आप ऐप वाले को जिंदगी भर कमीशन दे रहे हो ताकि वो आपका पैसा एक मैनेजर को दे, जो फिर आपका पैसा किसी और मैनेजर को दे दे। हर कोई अपना कट ले रहा है। जब तक रिटर्न आप तक पहुंचता है, कुछ बचता ही नहीं है।

The hard truth? You are basically paying for these fund houses' fancy marketing budgets using your own retirement money. It's time to wake up.कड़वा सच? आप असल में अपने रिटायरमेंट के पैसे से इन फंड हाउस के फैंसी मार्केटिंग बजट की भरपाई कर रहे हो। अब तो जाग जाओ यार।

How to Stop Getting Fooledबेवकूफ बनने से कैसे बचें

Before you invest another rupee, please go check your portfolio right now:एक भी रुपया और लगाने से पहले, जरा अपना पोर्टफोलियो चेक कर लो:

Look for the Word "Fund": If your mutual fund just holds a bunch of other mutual funds, congratulations, you're in an FoF."फंड" शब्द ढूंढो: अगर आपका म्यूचुअल फंड बस दूसरे म्यूचुअल फंड्स खरीद कर बैठा है, तो बधाई हो, आप FoF में फंसे हो।

Check for "Regular": If your statement says "Regular" instead of "Direct", your app is secretly taking a commission from your pocket every single month."रेगुलर" चेक करो: अगर आपके स्टेटमेंट में "डायरेक्ट" की जगह "रेगुलर" लिखा है, तो समझो ऐप हर महीने आपकी जेब काट रहा है।

Cut the Middleman: If you want gold, just buy a Gold ETF directly. Stop paying extra layers of fees just because a pretty app told you to.बिचौलियों को हटाओ: अगर सोना चाहिए, तो सीधे जाकर गोल्ड ईटीएफ (Gold ETF) खरीदो। सिर्फ इसलिए एक्स्ट्रा फीस मत दो क्योंकि किसी सुंदर से ऐप ने आपको ऐसा करने को कहा था।

Stop paying someone to hold an umbrella for you when you can just stand under a roof. Check your portfolio, dump the 'Regular' plans, and stop letting 'convenience' drain your bank account!जब आप खुद छत के नीचे खड़े हो सकते हो, तो किसी को छाता पकड़ने के पैसे देना बंद करो। अपना पोर्टफोलियो चेक करो, ये 'रेगुलर' प्लान्स हटाओ, और 'सुविधा' के नाम पर अपना बैंक अकाउंट खाली करवाना बंद करो!

Frequently Asked Questions (FAQs)अक्सर पूछे जाने वाले प्रश्न (FAQs)

1. What exactly is the "double fee" in a Fund of Funds?1. "फंड ऑफ फंड्स" में ये "डबल फीस" का क्या चक्कर है?▼

When you buy a standard mutual fund, you pay one management fee (the expense ratio). When you buy a Fund of Funds, you pay a fee to the FoF manager, and you pay the fees of all the underlying funds they buy with your money. For example, if you buy the Axis Gold Fund, you are paying around 0.18% just for the wrapper, plus the ~0.54% expense ratio of the underlying Axis Gold ETF it invests in. You are paying twice for the exact same asset.जब आप नॉर्मल म्यूचुअल फंड लेते हो, तो एक मैनेजमेंट फीस देते हो। पर जब आप FoF लेते हो, तो आप FoF वाले मैनेजर को भी फीस देते हो, और उन सारे फंड्स की भी फीस देते हो जो वो आपके पैसे से खरीदते हैं। मतलब, एक्सिस गोल्ड फंड लेने पर आप 0.18% फीस सिर्फ उस डब्बे की दे रहे हो, और अंदर के एक्सिस गोल्ड ETF की 0.54% फीस अलग से। एक ही चीज़ के दो बार पैसे दे रहे हो आप।

2. If I buy a FoF on a popular payment app like PhonePe, is it really that bad?2. अगर मैं PhonePe जैसे ऐप से FoF लूं, तो क्या सच में इतना नुकसान है?▼

Yes. Most convenience-first apps default you to Regular Plans. This means you are paying the double-fee layer of the FoF plus a distributor commission of up to 0.50% (or more) every single year. You could be bleeding over 1.2% annually in total costs just to hold something as basic as gold. Over a 10-year period, that fee drag will severely cripple your compounding.हां भाई, बहुत बुरा है। ये ऐप्स आपको "रेगुलर प्लान" चिपका देते हैं। मतलब FoF की डबल फीस तो आप दे ही रहे हो, ऊपर से ऐप वाले को भी हर साल 0.50% तक कमीशन दे रहे हो। बस सोना रखने के लिए आप साल का 1.2% पैसा बर्बाद कर रहे हो। 10 साल में ये आपकी सारी कम्पाउंडिंग की वाट लगा देगा।

3. Why do mutual fund houses (AMCs) even create FoFs if they are so inefficient for me?3. जब FoF इतने बेकार हैं तो ये म्यूचुअल फंड वाले इन्हें बनाते ही क्यों हैं?▼

Because they are highly efficient for them. FoFs allow AMCs to attract retail investors who don't have Demat accounts. It is a marketing vehicle designed to funnel more capital into their existing ETFs, allowing the AMC to collect an extra layer of management fees for doing virtually zero additional work.क्योंकि उनके लिए ये बहुत फायदेमंद हैं! FoF से वो उन लोगों को फंसाते हैं जिनके पास डीमैट अकाउंट नहीं है। ये बस उनके बाकी फंड्स में पैसा लाने का एक जुगाड़ है, जिससे वो बिना कुछ किए आपसे एक्स्ट्रा फीस ऐंठ सकें।

4. Does the fund manager of an FoF actually do any real "managing"?4. क्या FoF का मैनेजर सच में कोई दिमाग लगाता है या "मैनेजमेंट" करता है?▼

In most cases, absolutely not. If you look at an AMC's Gold FoF, the manager simply takes your money and dumps it into their own company's ETF. There is no active stock picking, no complex analysis, and no "alpha" generated. You are paying a high-priced management fee for someone to execute a basic buy order that a free automated script could do.ज्यादातर बिल्कुल नहीं। गोल्ड FoF में वो बस आपका पैसा लेता है और अपनी ही कंपनी के ETF में डाल देता है। ना कोई स्टॉक चुनता है, ना कोई रिसर्च। आप इतनी भारी फीस बस इसलिए दे रहे हो कि कोई वो काम करे जो कंप्यूटर फ्री में कर सकता है।

5. How do I find out if I am secretly invested in an FoF?5. मुझे कैसे पता चलेगा कि मैंने गलती से कोई FoF तो नहीं ले रखा?▼

Open your investing app and check the "Holdings" or "Portfolio" section of your mutual fund. If the top holdings are listed as other mutual funds or ETFs (e.g., "Axis Gold ETF - 100%") instead of actual company stocks or physical bonds, you are stuck in a Fund of Funds wrapper.अपना ऐप खोलो और फंड की "Holdings" चेक करो। अगर वहां स्टॉक्स या बांड्स की जगह कोई दूसरा म्यूचुअल फंड या ETF (जैसे "Axis Gold ETF - 100%") लिखा है, तो समझ जाओ आप FoF के जाल में फंस चुके हो।

6. What is the smartest, most cost-effective alternative to a Fund of Funds?6. FoF से बचने का सबसे स्मार्ट और सस्ता तरीका क्या है?▼

Cut out the middlemen entirely. If your FoF invests in an index or a commodity, just buy the direct ETF counterpart yourself. Instead of an expensive Gold FoF or Nifty FoF, simply log into your broker and buy Gold BeES or Nifty BeES. You will instantly eliminate the FoF wrapper fee and keep your compounding returns in your own pocket.बीच वाले लोगों को हटाओ। सीधे खुद ही ETF खरीद लो ना! महंगे गोल्ड FoF या निफ्टी FoF लेने की जगह, बस ब्रोकर ऐप पर जाओ और Gold BeES या Nifty BeES खरीद लो। फालतू की फीस बच जाएगी और सारा मुनाफा आपका होगा।

7. Why did my financial advisor or bank manager strongly recommend a Fund of Funds?7. फिर मेरे बैंक वाले या एडवाइजर ने मुझे FoF लेने को क्यों कहा था?▼

Trailing commissions. When they sell you a "Regular" FoF, they get a percentage of your total investment value every single year, for as long as you hold the fund. They aren't recommending it because it's the optimal vehicle for your wealth; they are recommending it because it secures a lifetime passive income stream for them at your expense.कमीशन के लालच में! जब वो आपको "रेगुलर" FoF बेचते हैं, तो उन्हें हर साल आपके पैसे पर कमीशन मिलता रहता है, जिंदगी भर! वो इसलिए नहीं बता रहे क्योंकि ये आपके लिए अच्छा है; वो इसलिए बता रहे हैं क्योंकि इससे उनकी जेब भर रही है।

8. "But I don't have a Demat account. Isn't the convenience of an FoF worth the extra fee?"8. "पर मेरे पास तो डीमैट अकाउंट ही नहीं है। क्या सुविधा के लिए थोड़ी फीस देना ठीक नहीं है?"▼

No. Opening a Demat account with a discount broker in India today takes about 10 minutes and is virtually free. By choosing an FoF simply to "save time," you are volunteering to surrender lakhs of rupees in compounding fees over a 10 to 15-year horizon. You are paying an outrageously high price for a 10-minute shortcut.बिल्कुल नहीं। आज भारत में डीमैट अकाउंट खोलने में बस 10 मिनट लगते हैं और वो भी फ्री में। बस 10 मिनट बचाने के चक्कर में आप अगले 10-15 सालों में लाखों रुपये का नुकसान करवाने को तैयार हो? ये शॉर्टकट बहुत महंगा पड़ने वाला है।

9. What about International Funds of Funds? Are they a trap too?9. इंटरनेशनल फंड्स (International FoFs) का क्या? क्या वो भी धोखा हैं?▼

Yes, they are notoriously expensive. An Indian AMC will collect an expense ratio to pool your money, only to forward it to an offshore fund (like a US tech ETF) which also charges its own fee. Add in the hidden costs of currency conversion spreads, and your global returns are handicapped before the market even opens. It is a highly inefficient way to get foreign exposure.हां यार, वो भी बहुत महंगे पड़ते हैं। एक इंडियन कंपनी फीस लेगी, फिर वो पैसा किसी विदेशी फंड (जैसे US टेक ETF) को देगी, वो अपनी अलग फीस लेगा। ऊपर से करेंसी बदलने का चार्ज! मार्केट खुलने से पहले ही आपका रिटर्न आधा हो जाता है। बाहर इन्वेस्ट करने का ये बहुत ही घटिया तरीका है।

10. If I realize I am stuck in an FoF right now, should I exit immediately?10. अगर मुझे अभी पता चला कि मैं FoF में फंसा हुआ हूं, तो क्या मुझे तुरंत बेच देना चाहिए?▼

Run the numbers, but the answer is almost always yes. Ripping the band-aid off might trigger a small exit load (often 1% if sold within a short window) or some short-term capital gains tax. However, taking a one-time tax hit to move your capital into a direct, low-cost ETF is mathematically far superior to letting a bloated, double-layered expense ratio bleed your portfolio dry for the next two decades.कैलकुलेशन करके देखो, पर जवाब लगभग हमेशा 'हां' ही होगा। निकालने पर थोड़ा बहुत टैक्स या एग्जिट लोड (exit load) लग सकता है। लेकिन एक बार टैक्स भर के किसी सस्ते और डायरेक्ट ETF में पैसा डालना, अगले 20 साल तक डबल फीस में अपना पैसा लुटवाने से हजार गुना बेहतर है।

I believe that knowledge is the ultimate currency. Through Deep Money Minds, I bridge the gap between complex financial concepts and everyday practical technology to help you succeed.मेरा मानना है कि ज्ञान ही सबसे बड़ी संपत्ति है। दीप मनी माइंड्स के माध्यम से, मैं आपको सफल होने में मदद करने के लिए जटिल वित्तीय अवधारणाओं और रोजमर्रा की व्यावहारिक तकनीक के बीच की खाई को पाटने का काम करता हूँ।