Guide

How to use the inflation calculator

Three steps, under 30 seconds — no sign-up, no button to click. The result updates as you type.

1

Enter an amount and pick a year

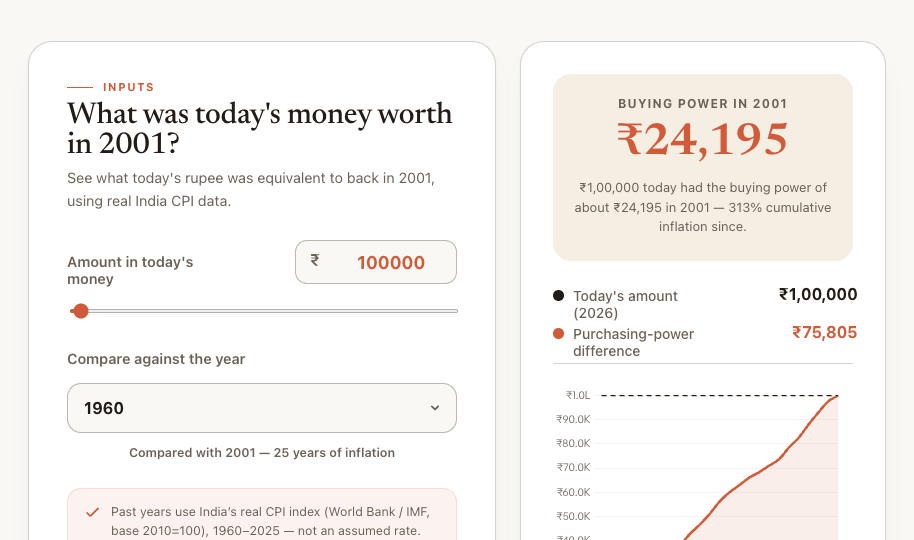

Type the amount in today's money, then choose any year from 1960 to 2075. For a past year, the tool uses India's real CPI data to show what that money was worth back then.

2

Read the result and year-by-year table

See the equivalent value, the purchasing-power difference, and total inflation over the period. The schedule table below breaks it down year by year, with the actual CPI index and year-on-year change.

3

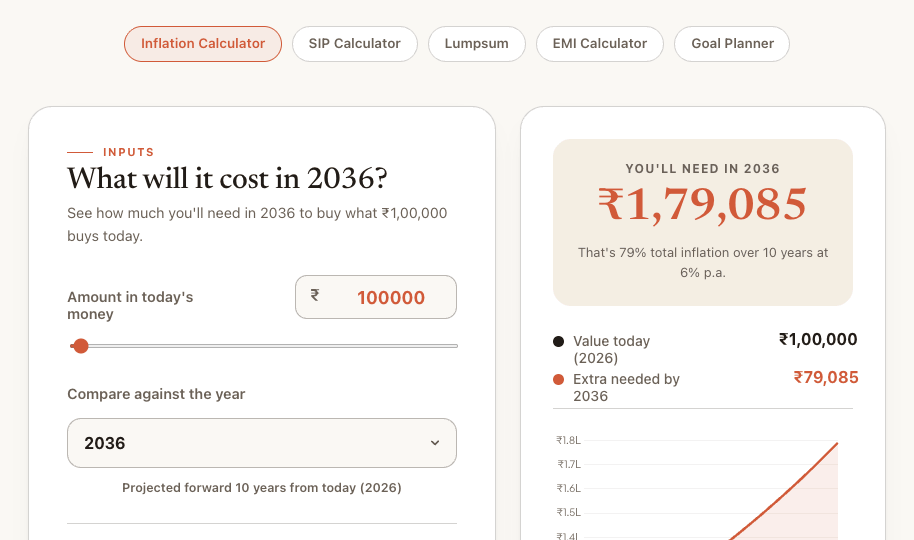

Project into the future

Pick a future year and an assumed inflation rate appears. See exactly how much you'll need later to buy what your money buys today — ₹1,00,000 becomes ₹1,79,085 in 10 years at 6%.